================================================================================

Mean vector

$$$E[X] \\

= [E[X_1], E[X_2], \cdots, E[X_N]]^T \\

= [\mu_1,\mu_2,\cdots,\mu_N]^T \\

= \pmb{\mu}$$$

* $$$E[X]$$$: Mean vector

================================================================================

Covariance matrix:

(1) represents relationship between features of each dimention as covariance (off-diagonal regions)

(2) represents variance of features in each dimenstion as variance (diagonal axis positions)

================================================================================

$$$COV[X] \\

= \Sigma \\

= E[(X-\mu)(X-\mu)^T] \\

= \begin{bmatrix}

E[(x_1-\mu_1)(x_1-\mu_1)^T]&&\cdots&&E[(x_1-\mu_1)(x_N-\mu_N)^T]\\

\cdots&&\cdots&&\cdots\\

E[(x_N-\mu_N)(x_1-\mu_1)^T]&&\cdots&&E[(x_N-\mu_N)(x_N-\mu_N)^T]\\

\end{bmatrix} \\

= \begin{bmatrix}

\sigma_1^2&&\cdots&&C_{IN}\\

\cdots&&\cdots&&\cdots\\

C_{IN}&&\cdots&&\sigma_{N}^2\\

\end{bmatrix}$$$

* $$$C_{IN}$$$: covariance between ith and Nth

================================================================================

Characteristics of covariance

- $$$x_i$$$, $$$x_k$$$ increase together, covariance value $$$c_{ik}>0$$$

- $$$x_k$$$ increases, $$$x_i$$$ decreases, covariance value $$$c_{ik}\lt 0$$$

- $$$x_i$$$ and $$$x_k$$$ are uncorrelated, covariance value $$$c_{ik} = 0$$$

- $$$|c_{ik}| \lt \sigma_i\times \sigma_k$$$, $$$\sigma_i$$$ is std of $$$x_i$$$

- $$$c_{ii} = \sigma_i^2 = VAR(x_i)$$$

================================================================================

* $$$\rho_{ik}$$$: correlation coefficient

(1) $$$-1\le \rho_{ik}\le 1$$$

(2) $$$\rho_{ik}=-1$$$: highest negative correlation

(2) $$$\rho_{ik}=1$$$: highest positive correlation

* $$$c_{ik} = \rho_{ik} \sigma_i\sigma_k$$$

* $$$\rho_{ik}=\dfrac{c_{ik}}{\sigma_i\sigma_k}$$$

================================================================================

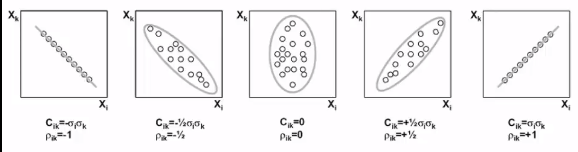

* Each circle: each sample data

================================================================================

(1) $$$X_1$$$ decreases and $$$X_k$$$ increases

* $$$c_{ik}=-\sigma_i \sigma_k$$$

* $$$\rho_{ik}=-1$$$

(2) $$$X_1$$$ decreases and $$$X_k$$$ increases

* $$$c_{ik}=-\frac{1}{2} \sigma_i \sigma_k$$$

* $$$\rho_{ik}=-\frac{1}{2}$$$

(3) $$$X_1$$$ and $$$X_k$$$ are uncorrelated

* $$$c_{ik}=0$$$

* $$$\rho_{ik}=0$$$

* Each circle: each sample data

================================================================================

(1) $$$X_1$$$ decreases and $$$X_k$$$ increases

* $$$c_{ik}=-\sigma_i \sigma_k$$$

* $$$\rho_{ik}=-1$$$

(2) $$$X_1$$$ decreases and $$$X_k$$$ increases

* $$$c_{ik}=-\frac{1}{2} \sigma_i \sigma_k$$$

* $$$\rho_{ik}=-\frac{1}{2}$$$

(3) $$$X_1$$$ and $$$X_k$$$ are uncorrelated

* $$$c_{ik}=0$$$

* $$$\rho_{ik}=0$$$